Blog

Housing inventory challenges across South Florida

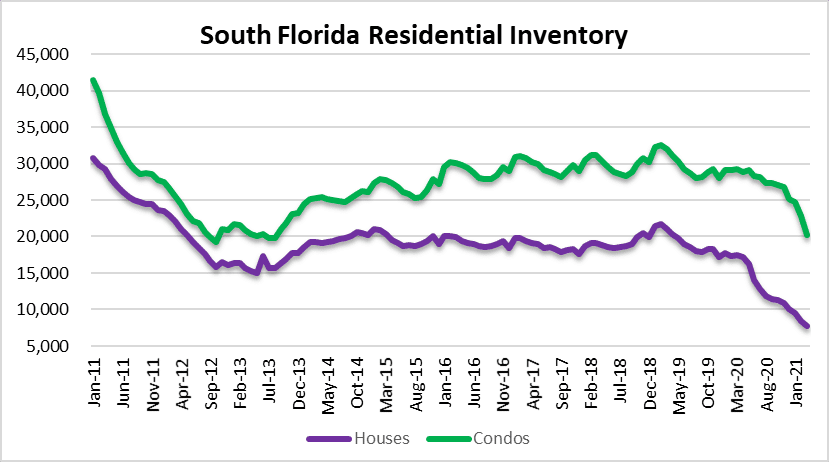

Housing inventory continued to drop across South Florida during the month of March. At the end of the month there were only 7, 711 houses available for sale in the Tri-County area and 20,251 condo properties available for sale. These are once again setting new lows as far as single-family homes are concerned and it looks like the condo inventory is reaching levels that we haven’t seen since 2012 to 2013. The most recent low for condos during the last cycle was in October 2012 when there were 19,229 units available for sale. In May 2013 the single-family home inventory bottomed-out at 15,056 before it started to climb again. For some additional perspective, during the last housing crash there were a total of 72,241 houses in condos on the market in January 2011. Last month there was only a fraction of that available with a total number of 27, 962 houses and condos available for sale.

With minimal inventory available across Miami Dade, Broward, and Palm Beach markets prices continued to climb. The average sale price of a single-family home in the Tri-County area reached a whopping $900,652 during the month of March. The average sale price of a condo property reached $446,179 last month. When will the madness stop? Is the housing bubble getting ready to pop again? If so, what will be the catalyst this time around? The last housing bubble popped because of easy money / subprime debt fueling ridiculous prices. Something to keep an eye on is this time around is the rising cost of insurance.

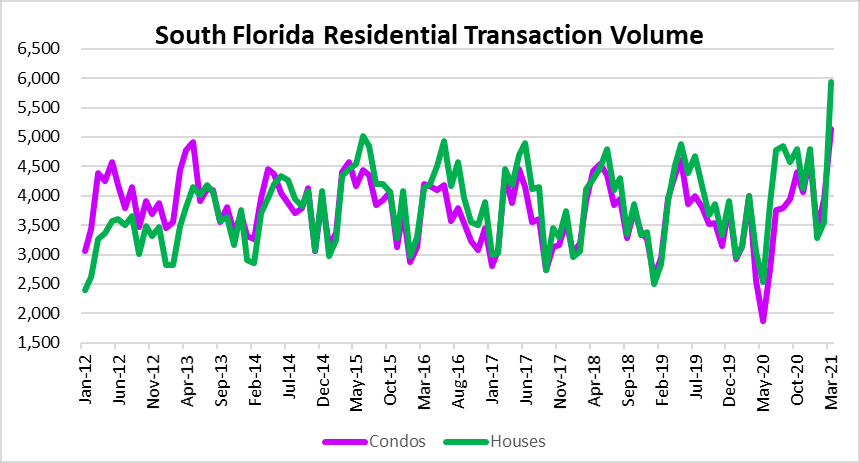

Even with minimal inventory available for sale, deal volume spiked during the month of March for a total of 11,073 sold units of houses and condos. Out of that number, 5,143 houses were sold and 5,930 condo properties were sold. When you look at the monthly averages going back to 2012, this year it’s starting out pretty strong after seeing the numbers in March. What’s crazy is that we are really running out of properties to sell. Is there a chance we will reach zero houses for sale over the next few months, or will inventory reverse and start to climb?

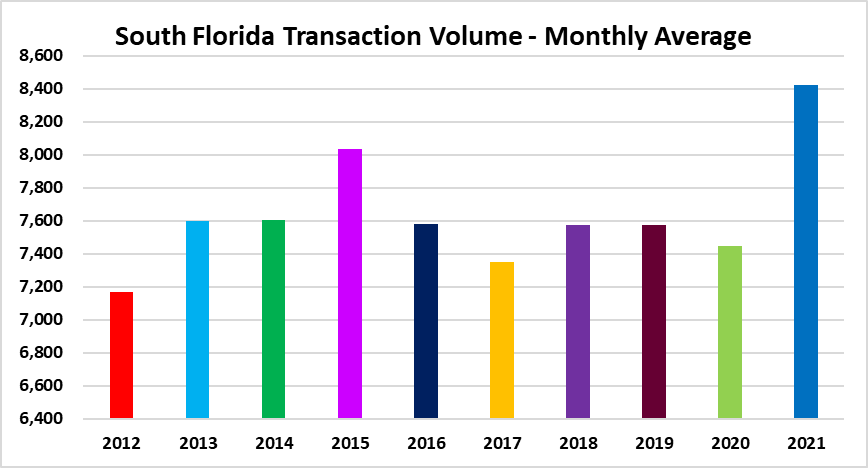

| Year | Monthly Average | |||

| 2012 | 7,167 | |||

| 2013 | 7,598 | |||

| 2014 | 7,603 | |||

| 2015 | 8,034 | |||

| 2016 | 7,581 | |||

| 2017 | 7,352 | |||

| 2018 | 7,573 | |||

| 2019 | 7,572 | |||

| 2020 | 7,446 | |||

| 2021 | 8,423 | |||

Mortgage rates

We always include a chart of the latest mortgage rates in our market outlook. After bottoming out over the summer, rates had a modest rebound and may be heading higher. It would take a big move (at least one half percentage point) to impact real estate prices. In the past we have noted that a 5.00% 30-year mortgage is the line in the sand. The only time we reached that level in the last decade was in 2018 (very briefly). As long as money is this cheap it will continue to keep real estate prices elevated.

This market outlook covers real estate activity in Miami-Dade, Broward and Palm Beach County, Florida. Here are just a few of the cities in each of these three markets:

- Miami-Dade – Aventura, Coral Gables, Miami Beach, Hialeah, Sunny Isles Beach, North Miami, Homestead and Key Biscayne.

- Broward – Fort Lauderdale, Pompano Beach, Deerfield Beach, Hollywood, Hallandale, Weston, Parkland and Lighthouse Point.

- Palm Beach – Delray Beach, Highland Beach, Jupiter, Boynton Beach, Boca Raton and Lake Worth.