Blog

Mortgage foreclosure activity in South Florida

The trend in South Florida mortgage foreclosure filings so far in 2016 appears to be moving higher. We have repeatedly discussed how keeping rates too low for too long will eventually have consequences. Real estate prices may have been propped-up temporarily, but the underlying problems in the market remain. Here are a few charts of the current foreclosure activity in the tri-county area:

Mortgage Foreclosure Filings in South Florida

- In April there were 1,411 new mortgage foreclosure filings in South Florida

- The 2015 monthly average was 796 filings per month

- The 2016 monthly average is 1,230, representing a whopping 54% increase over last year

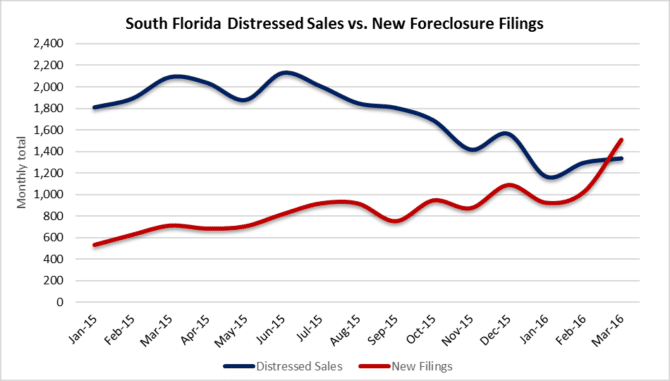

Mortgage Foreclosure Filings compared to Distressed Sales

This next chart compares foreclosure filings to the pace of distressed property sales. During the month of March the 1,511 foreclosure filings in the South Florida surpassed the 1,339 distressed sales. We haven’t seen filings exceed distressed sales in years and it’s certainly not a good sign for a housing market in the eighth year of a “recovery”.

Mortgage Foreclosure Filings in Miami-Dade County

- In April there were 523 new filings, down slightly from March

- The 2015 monthly average was 387

- The 2016 monthly average is 523, representing a 35% increase over last year

Mortgage Foreclosure Filings in Broward County

- In April there were 575 new filings

- The 2015 monthly average was 280

- The 2016 monthly average is 436, representing a 56% increase over last year

Mortgage Foreclosure Filings in Palm Beach County

- In April there were 313 new filings

- The 2015 monthly average was 142

- The 2016 monthly average is 271, representing a 91% increase

Summary

As the pace of new foreclosure filings climbs, South Florida continues to wrestle with a large inventory of distressed properties left over from the last bubble. Florida is a judicial state and the average residential foreclosure takes over 1,000 days to complete. Believe it or not, many of the existing properties in foreclosure started the process back in 2008. The Fed drastically reduced interest rates in 2009 to rescue the economy and created yet another bubble by keeping rates too low for too long. Apparently they believe you can repair damages from one bubble by creating a new one. The economy remains sluggish at best and cracks in the market are beginning to show. It will be interesting to see how the next real estate market correction plays out and it may be here sooner than you think.