Blog

What’s new in the South Florida residential market?

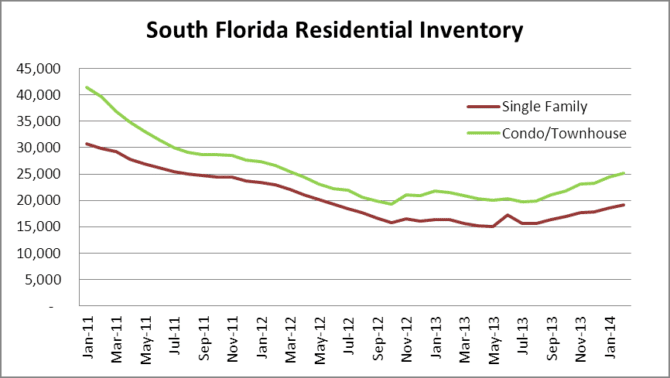

Today we will take a look at some of the charts and data for Miami-Dade, Broward and Palm Beach County, Florida. First, we will take a look at the gradual increase in residential inventory.

The month of February showed at total of 44,372 residential properties listed for sale in the tri-county area. This is an inventory level that we haven’t seen in two years. The gradual increase is a positive trend for buyers who have grown tired of getting priced out of the market. It certainly appears that this trend will continue throughout 2014.

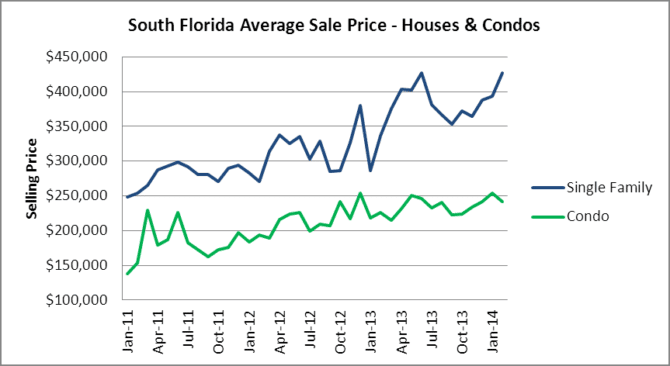

Next, here is a snapshot of the average sale price of houses and condo/townhouse properties in the tri-county area.

The average sale price of a single-family home in South Florida reached $426,755 in February and the average sale price of a condo/townhouse dipped slightly to $241,576. The average sale prices can be volatile because one or two high-end properties can sway the averages. In one of our next posts we will take a look at the median prices that show less volatility.

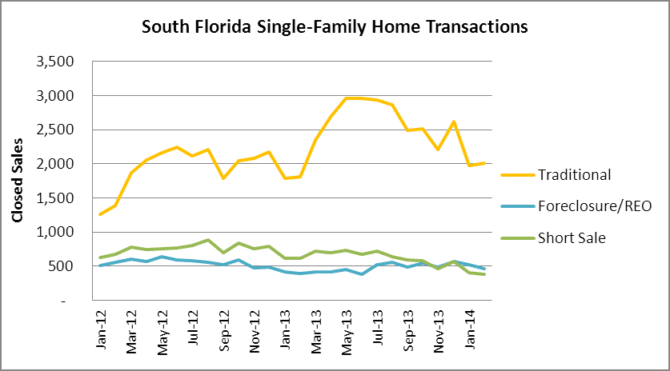

What types of transactions are closing? Here is a chart of single-family home sales through February.

Out of 2,859 single-family home transactions that closed in February, here is the breakdown:

- There were 2,017 traditional sales which accounted for 71% of all closings.

- There were 459 foreclosure/REO sales which accounted for 16% of all closings.

- There were 383 short sales that account for the remaining 13% of all closings.

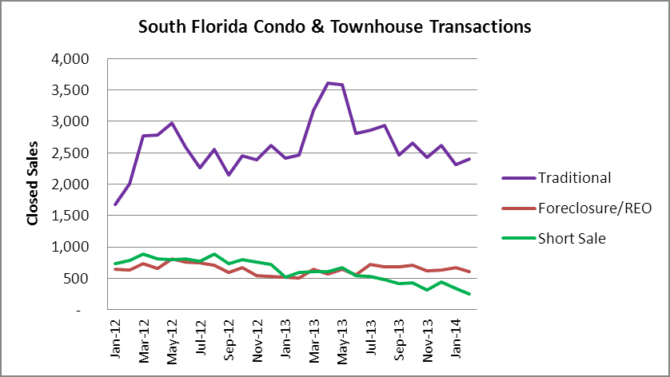

Now for a look at the condo/townhouse deals.

There were 3,266 closings in the condo/townhouse segment in February and here is the breakdown of closings:

- There were 2,407 traditional sales which accounted for 74% of all closings.

- There were 609 foreclosure/REO sales which accounted for 18% of all closings.

- There were 250 short sales which accounted for the remaining 8% of all closings.

It is important to note the drop in the short sale transactions, as the mortgage-debt forgiveness act expired at the end of 2013, so most people had them completed by then. If they didn’t get the transaction closed by the end of the year, there really isn’t much incentive to do a short sale now and most distressed borrowers will let their properties go into (or remain in) foreclosure.

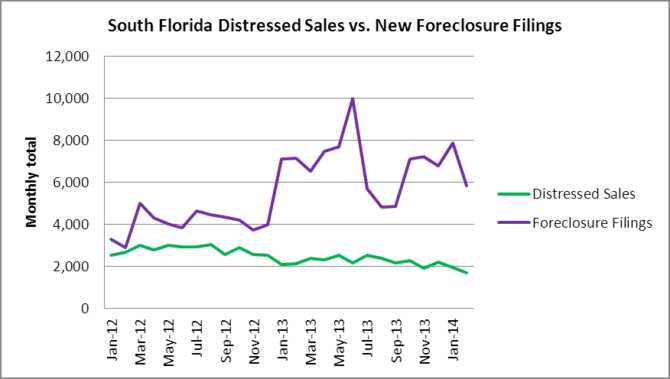

Finally, February showed some improvement in the level of new foreclosure filings compared to the amount of distressed sales. One month certainly does not make a trend, but this is a start. Ideally, it would be nice to have the “distressed sales” line closer to the “foreclosure filings” line in order to decrease (or not contribute to) the massive shadow inventory of foreclosures, but this past month showed some improvement.