Blog

Looking to strike a deal on a foreclosure? Submit an offer that will get accepted by the lender!

Looking to strike a deal on a foreclosure? Make sure that you submit an offer that will get accepted by the lender!

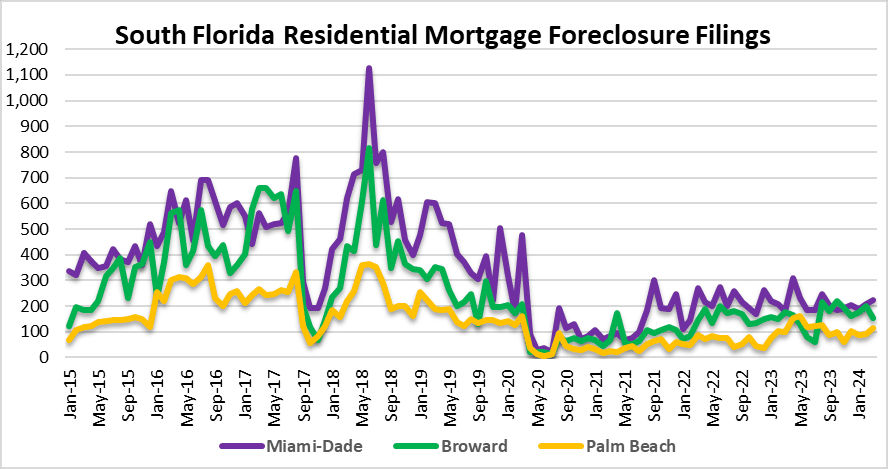

After viewing our latest foreclosure filing data, the South Florida housing market and other bubbly markets could start to see the next wave of bank owned (REO) properties. Although there hasn’t been a large spike in mortgage foreclosure filings, it looks like a base is building in the monthly activity and the insurance crisis will certainly play a role. The properties may not enter the market in a deluge as they did in the last crisis, but the banks may gradually sell their inventory over the next several years now that prices have rebounded. Either way, it is important that REO offers are formatted properly in order to streamline the process and conform to seller requirements. Below are some helpful tips:

- Visit the property and conduct a basic inspection prior to making an offer. If you don’t plan to make repairs yourself, it is best to bring your contractor with you on the pre-inspection visit. You certainly want to be aware of any major issues prior to making the offer and it is best not to commit escrow funds on a property that may not pass this pre-inspection.

- Understand any existing issues that you may inherit once you close on the property. These include structural problems, plumbing and electrical issues and potential code violations that haven’t been cited (yet) from illegal additions to the property or repair work that is not up to code.

- Use an As-Is Contract to keep things simple. Banks rarely want to allow repair allowances and they typically provide a Seller’s Addendum / Counter Offer that will state as such.

- Provide proof of funds if paying cash and loan pre-approval from a lender, (not a broker) if financing. Make sure any proof of funds submitted matches the entity or person on the contract.

- If you are buying in the name of a corporation or LLC, you should provide a copy of the entity record from the State of Incorporation / Organization. The Seller will often request a certificate of good standing from the state, so you may want to have that in advance of preparing an offer.

- Put your money where your contract is: If you are serious about closing on the property, you should have no problem making a sizeable escrow deposit. I tell most of my clients to make an initial deposit of 10% especially on cash offers. If you plan to close in a few weeks, this should not be a problem.

- Submit a copy of the escrow deposit payable to seller’s escrow agent. REO transactions (especially cash deals), usually close within 2 weeks and an extra title company usually slows the process down. In some markets, the Seller’s agent must have possession of the deposit check prior to submittal of any offer.

- Changes to Seller’s Addendum / Counter Offer are not acceptable, so don’t bother marking it up when you get it. The seller will usually reject any changes and move on to the next offer.

- All offers should be “highest and best” when you submit them, that way you won’t be let down if your offer isn’t accepted.

- If you are working with a buyer’s agent, make sure they follow the instructions provided by the Seller’s agent. I post a checklist just like this one online to make sure the offer gets submitted quickly.

- Minimize contingencies when presenting offers to a bank. The listing agent and the asset manager will do a side-by-side offer comparison and will select the deal that yields the highest price along with a quick, seamless closing.

Finally, just because the property is a foreclosure does not mean that it is priced correctly or a good deal. Do your own homework and valuation by using (3) comparable active listings and (3) comparable closed sales from the same neighborhood as the subject. The closed sales are the most important, so if you have a few within the last 60-90 days that would be great. If you don’t have access to the MLS, you can always search closed sales on the property appraiser’s website or Zillow.

This real estate market outlook covers real estate activity in Miami-Dade, Broward and Palm Beach County, Florida. Here are just a few of the cities in each of these three markets:

- Miami-Dade – Aventura, Coral Gables, Miami Beach, Hialeah, Sunny Isles Beach, North Miami, Homestead, Doral, Miami Lakes, Downtown Miami, Brickell and Key Biscayne.

- Broward – Fort Lauderdale, Pompano Beach, Deerfield Beach, Hollywood, Hallandale, Weston, Parkland, Wilton Manors, Oakland Park, Plantation, Cooper City, Davie, Coral Springs, Sea Ranch Lakes, Lauderdale by the Sea and Lighthouse Point.

- Palm Beach – Delray Beach, Highland Beach, Jupiter, Palm Beach Island, Boynton Beach, Boca Raton, Highland Beach, Palm Beach Gardens, West Palm Beach, Wellington and Lake Worth.