Blog

Recent single-family housing inventory, data and pricing trends for Fort Lauderdale, Florida

Well, after the June housing data was released, it looks like much of the same for the single-family market in the greater Fort Lauderdale market. The available inventory currently on the market has dropped again, now standing at a mere 3,045 homes at the end of July 2012, down from 6,451 back in September of 2010. With the available supply of homes chopped in half over the past two years, you can now see the dramatic impact that the halt of foreclosures has done to the South Florida housing market. Demand appears stronger than it actually is because buyers are looking at such a small sample of available properties. This trend will eventually turn and supply will return to the market as the occupants that have been living for free for the past 2-3 years and not making payments will eventually have to vacate and pay for a place to live. Sounds crazy, doesn’t it?

The average sale price is bumping around and hasn’t really made a move that looks like the start of a new trend in awhile, as shown in the chart below. February through May 2012 looked like it was heading upward, but we could be heading back down as additional short sales get approved and sold.

I guess the only new data point that could be starting a new trend is the slight uptick in distressed sales. After three consecutive months of 15% of all single family property sales being distressed sales (REO or short sale), that percentage popped-up to 16% in July 2012. My prediction has been that this number will continue to increase as most banks are approving short sales at a faster clip after the robo-signer settlement and will gradually get their foreclosure operations moving along.

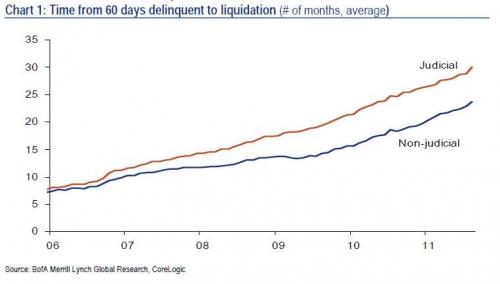

People keep asking me: “But when will these foreclosures finally hit the market?” The state of Florida is what is know as a judicial state, which means that all foreclosures must go through the court process to be completed, and they meet several hurdles and bogus borrower lawsuits and bankruptcies, etc. along the way. To put it in perspective, the Chart below from Bank of America / Merrill Lynch and Corelogic show that foreclosures in judicial states like Florida take on average 30 months to complete after the borrow is 60-days late, and that is about 10-12 months longer than non-judicial states. Now you can see why there are thousands of Floridians in there houses for over three years after the lis pendens was filed against them. Chilling-out, not paying a dime in mortgage, taxes, insurance or any housing related expenses, but somehow still taking plenty of vacations, paying their car payments and buying plenty of I-pads! Take a look at this chart:

Judicial States like Florida take over 30 months to complete foreclosures after a borrower is 60-days late on their mortgage.